Why Fraud Teams Should Care More About Authorizations Than Disputes

- March 16, 2026

- 0

- 5 min read

Sponsored Content

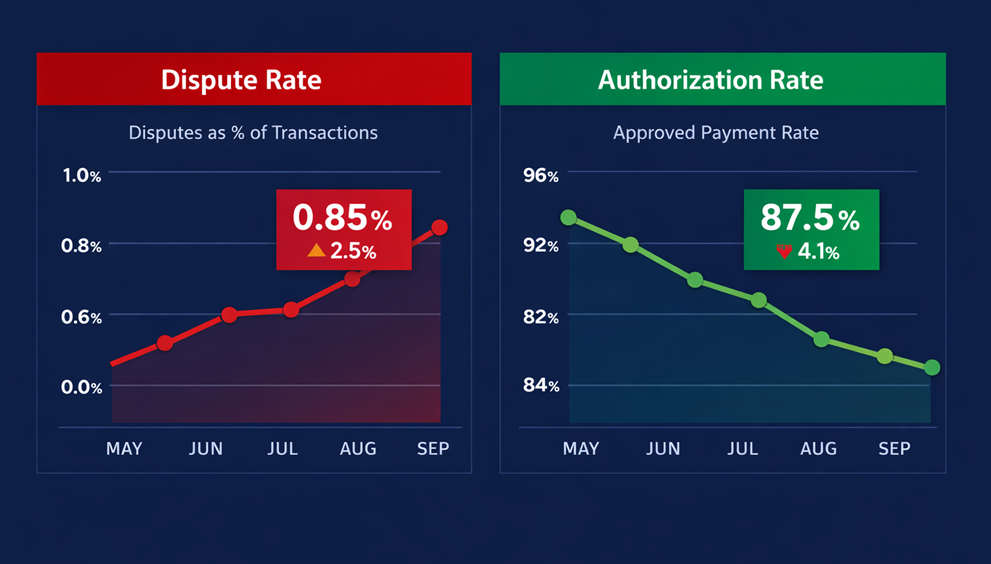

Fraud teams obsess over disputes. Network monitoring thresholds. Chargeback win rates. Prevention alert integrations. Ratio management. All are important.

But if disputes are your primary performance lens, you are optimizing against a lagging signal. Authorization is what sets the trajectory for a merchant’s processing portfolio.

By the time a chargeback arrives, the authorization decision is weeks old. The issuer has already scored the transaction. The behavioral pattern has already been logged. The customer has already formed an opinion about the experience.

Disputes are outcome reporting; they’re lagging signals. Authorization is where risk decisions are actually executed.

If fraud leaders want durable performance gains in 2026 and beyond, authorization strategy can’t be secondary to dispute management. It has to be seen as the control surface.

The Lag Problem

An institution’s chargeback rate is often used as a shorthand for fraud performance, but the dispute ratio does not actually give a clear picture of fraud.

Chargebacks reflect a composite signal that incorporates several factors: issuer interpretation, cardholder escalation behavior, additional friction for a merchant’s support team, billing descriptor clarity, and how the merchant responds to disputes. Notably, while fraud is one component, it does not define the whole picture.

More importantly, chargebacks are delayed. A dispute might appear 15 days after a purchase, or much later. In cases involving forward delivery, where a customer pays now but receives the product or service some time in the future, the dispute window can stretch much longer, sometimes up to 540 days.

Authorization decisions, by contrast, immediately shape approval rates, retry behavior, and issuer perception.

When fraud teams optimize primarily around dispute ratios, models often drift toward conservatism. That may reduce visible loss in the short term while quietly compressing approval rates and increasing retry intensity.

And that tradeoff isn’t theoretical.

Juniper Research estimates that false declines will cost merchants more than $264 billion globally by 2027. That number dwarfs many fraud-loss projections.

Fraud leaders rarely get fired for blocking too much. But the economic cost of over-blocking is measurable, and growing.

False Declines Are Not Neutral

False declines don’t automatically create disputes. But they do create behavioral distortion.

A declined customer retries. Maybe with the same card. Perhaps with a different one. Maybe they changed shipping details. Eventually, one attempt clears.

From a conversion standpoint, that looks like recovery.

From a behavioral standpoint, the transaction now carries velocity and variation signals that didn’t exist originally.

Issuers model anomaly patterns. Excessive retries and inconsistent signals increase scrutiny. That scrutiny doesn’t guarantee disputes, but in certain portfolios it correlates with higher post-transaction friction and reduced future approval stability.

Retry volatility is often the hidden variable between approval optimization and dispute instability. Aggressive orchestration can therefore solve today’s conversion problem while creating tomorrow’s volatility.

Authorization Shapes Portfolio Trajectory

Issuers assess merchants at the portfolio level. Approval stability, retry behavior, fraud reporting consistency, and dispute ratios all influence how future transactions are evaluated.

Merchants don’t control issuer models. But they do influence the inputs.

Stable authorization patterns produce predictable portfolio behavior. Volatility introduces uncertainty, and that changes how issuer models score future transactions.

This isn’t about “building trust” in a human sense. It’s about reducing statistical noise in your portfolio profile. Authorization quality affects how your next thousand transactions are treated, not just the one in front of you.

The Real Organizational Risk

In many companies, fraud and disputes are structurally disconnected. Fraud teams optimize fraud rates and false-positive rates. Dispute teams optimize win rate and monitoring exposure.

What’s rarely examined is lifecycle impact.

A rule that reduces fraud by 15 basis points but drops approval rate by 200 basis points may look successful in isolation. If that same rule increases retry volume and downstream dispute propensity, the net system effect may be negative.

Without integrated measurement, teams optimize locally.

Fraud reduction without authorization context is incomplete. Approval lift without dispute feedback is reckless.

The real opportunity is understanding how these systems influence each other instead of managing them separately.

AI Is Not the Limiting Factor

Most modern fraud stacks can support multi-objective optimization. The constraint is objective design, not model capability.

If your model is trained primarily against fraud rate, it will be biased toward safety. If it is trained against approval rate without dispute integration, it will be biased toward risk.

Balanced optimization requires incorporating fraud rates, approval rates, retry behavior, and dispute outcomes into the performance evaluation.

The problem isn’t inherent to machine learning; rather, the problem lies in how you initially train and evolve your AI agents as the work progresses.

What This Means Practically

Fraud teams don’t need to deprioritize disputes. They need to stop treating them as a primary performance signal. Approval rates and fraud rates should be tracked in tandem. Dispute outcomes should be segmented by authorization pathway. Retry intensity and behavioral volatility are more valuable when they are quantified as structured metrics.

If a rule improves fraud rate but degrades approval stability and increases retries, that tradeoff should be explicit. Otherwise, dispute ratios become the scoreboard for decisions made weeks earlier.

The Strategic Reality

Disputes measure what happened. Authorization shapes what will happen. If you only optimize what you can see in dispute data, you are optimizing on delay. Fraud performance is not just loss avoidance. It is portfolio trajectory management.

And portfolio trajectory is set at authorization.